The scale of the U.S. LNG export boom is unprecedented. From 2016 to 2023, U.S. export volumes surged by over 2,200%, establishing the nation as the world’s foremost LNG supplier.

This growth is underpinned by a massive infrastructure pipeline, with over 1,000 million tonnes per annum (MTPA) of new global export capacity in development, representing a potential capital investment of nearly $1 trillion.

A substantial portion of this capital is concentrated along the U.S. Gulf Coast, a region uniquely exposed to severe physical climate threats.

The convergence of escalating physical climate hazards, tightening regulations, and volatile market dynamics is transforming the risk landscape for U.S. LNG projects.

Once touted as a secure “bridge fuel,” the concentration of these multi-billion-dollar assets on the U.S. Gulf Coast now exposes them to a complex web of liabilities that threaten their operational uptime, financial viability, and social license to operate.

Physical Risks Now Deliver Multi-Week Revenue Shocks

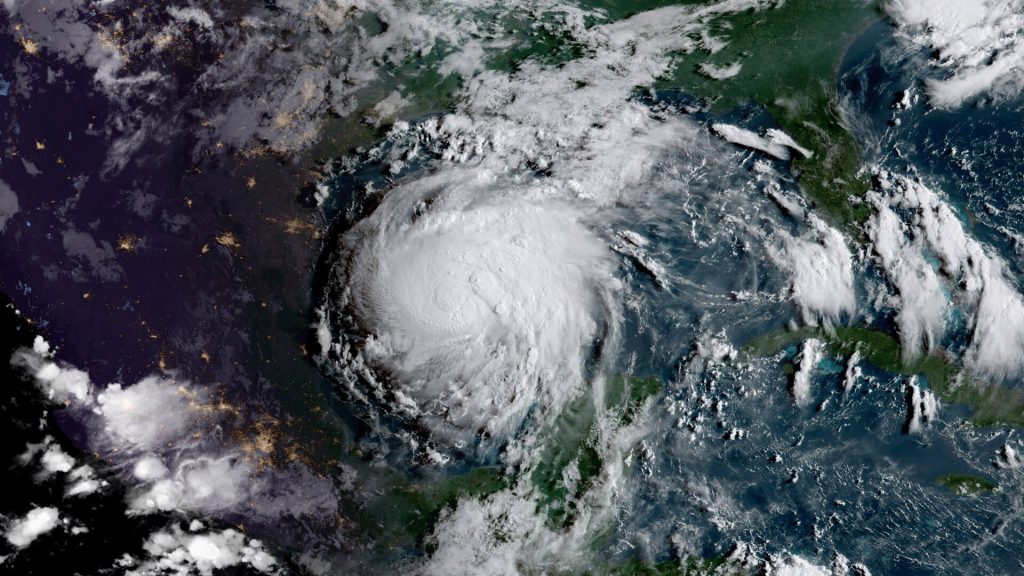

LNG terminals on the Gulf Coast are acutely vulnerable to intensifying climate impacts.

More frequent and powerful hurricanes are causing prolonged operational shutdowns, not primarily from direct asset damage, but from the failure of the regional power grid.

Hurricane Laura (2020) idled Cameron LNG for a month, and even a Category 1 storm, Hurricane Beryl (2024), knocked Freeport LNG offline for three weeks due to power loss.

Compounding this is the threat of accelerating sea-level rise, with the Gulf Coast expected to see a 23-inch rise by 2050, nearly double the national average, threatening facilities with severe flooding.

A Looming Supply Glut Threatens to Strand New Assets

The long-term economic viability of new LNG projects is under severe threat from a projected global supply glut expected after 2026.

Global liquefaction capacity is set to grow by a staggering 60% by 2030, creating a potential market surplus of 200 billion cubic meters (bcm).

This oversupply will depress prices and squeeze margins for U.S. producers, who face higher feedstock gas costs than competitors.

The International Energy Agency (IEA) projects that in its Stated Policies Scenario (STEPS), no new LNG supply may be needed globally until 2040 at the earliest, raising the specter of stranded assets for projects sanctioned in the mid-2020s.

Tightening Methane Regulations Are Bifurcating the Global Market

A shifting policy landscape is creating significant transition risks.

The EU’s Methane Regulation, effective August 2024, will impose stringent monitoring, reporting, and verification (MRV) requirements on LNG imports starting in 2027 and maximum methane intensity limits from 2030.

This is a critical challenge for U.S. exporters, as top-down satellite measurements suggest actual methane leakage rates are over four times higher than official EPA estimates, potentially eroding LNG’s climate advantage over coal.

Financing and Insurance Markets Are Recalibrating for Climate Risk

The financial community is responding to these mounting risks.

While capital is still available, traditional banks are becoming more cautious, with private credit filling the gap.

In contrast, the insurance market is showing signs of strain; in a landmark move, insurer Chubb reportedly ceased its $1.5 billion primary policy for the Calcasieu Pass LNG facility in May 2025, signaling that obtaining coverage for climate-vulnerable assets is becoming more difficult and expensive.

Environmental Justice Litigation Creates Tangible Financial Consequences

The LNG buildout is concentrated in “sacrifice zones” which are low-income communities and communities of color that bear a disproportionate burden of pollution and health risks.

This has fueled fierce community opposition and a wave of litigation that is derailing projects.

The D.C. Circuit Court of Appeals vacated FERC’s approvals for both the Rio Grande and Commonwealth LNG projects on environmental justice and climate grounds, causing significant delays and contributing to the withdrawal of financial backers like Sociétié Générale and Engie.

These legal and social risks are now a primary driver of project uncertainty and cost.

Physical Climate Threats

The concentration of U.S. LNG infrastructure on the Gulf Coast creates a systemic vulnerability to physical climate hazards.

A single major storm making landfall in the densely packed Texas-Louisiana corridor could impact approximately half of all U.S. LNG capacity, equivalent to about 12% of total U.S. gas consumption, with cascading effects on global energy markets.

Hurricanes & Storm Surge

The Gulf Coast is experiencing more frequent and intense major storms, posing a severe risk to LNG terminals.

Hurricane Laura in 2020, a Category 4 storm, brought a storm surge exceeding 15-17 feet to the Louisiana coastline.

This event caused a month-long shutdown of Cameron LNG and a week-long outage at Sabine Pass LNG.

More recently, Hurricane Beryl, a much weaker Category 1 storm, still forced a three-week shutdown of Freeport LNG in 2024.

These events demonstrate that even facilities not directly damaged can be idled for weeks by impacts to the surrounding region.

Sea-Level Rise

LNG terminals face an accelerating threat from sea-level rise (SLR) and coastal flooding. A federal NOAA study projects that the Gulf Coast will see a sea-level rise of 23 inches by 2050, nearly double the U.S. national average.

This is expected to cause more frequent and intense flooding, with potential inundation depths of up to 4 feet.

The risk is compounded by land subsidence and the loss of protective marshlands.

Some facilities may be relying on outdated risk assessments; for example, a 2012 assessment for Sabine Pass LNG used 1968 storm surge data, which likely underestimates current and future flood risk.

Peak-Load Spikes Cut Liquefaction Uptime

Extreme heat poses a multifaceted risk to LNG operations. High temperatures can reduce the efficiency of electric transmission lines and increase electricity demand for cooling, impacting operational capacity.

For the workforce, extreme heat is a direct safety threat, and the oil and gas industry has actively opposed federal rules to protect workers from heat-related illness.

The most critical vulnerability, however, is the regional power grid.

Prolonged power outages were the primary driver of the extended shutdowns at Cameron LNG after Hurricane Laura and Freeport LNG after Hurricane Beryl, highlighting a critical trade-off:

Terminal Exposure Matrix

The following table details the specific vulnerabilities and resilience measures for key U.S. Gulf Coast LNG terminals.

| Terminal Name | Location | Assessed Vulnerabilities | Resilience Measures |

|---|---|---|---|

| Cameron LNG | Hackberry, LA | Highly dependent on the regional power grid; Hurricane Laura caused a month-long shutdown due to power loss. | Facility is 8 feet above sea level with further elevated equipment. The company also built a stormproof community center. |

| Calcasieu Pass LNG | Cameron, LA | Located in an area hit by Hurricane Laura’s 17-foot storm surge. History of exceeding permitted emissions limits. | Protected by a flood barrier reported to be over 20 feet high. |

| Freeport LNG | Freeport, TX | Vulnerable to power outages (3-week shutdown from Hurricane Beryl), extreme cold (full shutdown in Feb 2021), and industrial accidents (explosion in June 2022). | Includes a protected marine berth and double-walled LNG storage tanks. |

| Golden Pass LNG | Near Sabine Pass, TX | Project is at least $2.4 billion over budget; main contractor filed for bankruptcy in March 2024. | A perimeter storm surge barrier has been installed with a finished elevation of 16 feet NGVD. |

| Sabine Pass LNG | Cameron Parish, LA | A 2012 environmental assessment relied on outdated 1968 storm surge data, likely underestimating current flood risk. | Specific resilience measures were not detailed in the provided context. |

| Port Arthur LNG | Port Arthur, TX | Located in a highly vulnerable region where existing hurricane protection systems are considered inadequate and were nearly overtopped during Hurricane Ike. | Project is under construction; specific resilience measures were not detailed. |

| Commonwealth LNG | Cameron, LA (Proposed) | Faces regulatory scrutiny and questions about cumulative flooding impacts due to proximity to other terminals. | Plans include a 26-foot levee and mitigating wetland loss through offset credits. |

| Rio Grande LNG | Brownsville, TX | Initial FERC approval was vacated by a court for inadequate climate and environmental justice study. South Texas location has lower hurricane risk than Louisiana. | Financing is tied to a large-scale Carbon Capture and Storage (CCS) project. |

Cost of Capital and Coverage is Rising

Financial and insurance markets are becoming increasingly cautious, tightening terms and raising costs for U.S. LNG projects as climate-related risks become more tangible.

Bank Retreat and Private Credit Influx

A notable trend is the partial retreat of traditional commercial banks from fossil fuel lending due to ESG pressures.

This has created an opening for private credit, which saw its deals in the oil and gas sector increase from $450 million in 2019-2021 to over $9 billion in 2021-2023.

However, major banks, particularly Japanese institutions like Mizuho and MUFG, remain significant financiers, with the sector receiving $121 billion from tracked banks in 2023.

Some European banks, like Sociétié Générale, have restricted financing for new LNG projects and withdrawn from specific projects like Rio Grande LNG over ESG concerns.

Insurance Market Tightening After Chubb Exit

The insurance market is also showing signs of strain. In a significant development in May 2025, major insurer Chubb reportedly ceased issuing its $1.5 billion primary policy for Venture Global’s Calcasieu Pass LNG facility.

Financing Climate-Exposed LNG Projects

| Project Name | Financing Status | Financing Details & Climate Factors |

|---|---|---|

| Rio Grande LNG | Secured (Phase 1) | Secured a record $18.4B financing package, aided by a commitment to a large-scale CCS project to capture over 5M tonnes of CO2 annually. |

| Golden Pass LNG | Under Construction / Financial Distress | Project is $2.4B+ over budget, and its main contractor filed for bankruptcy in March 2024, highlighting extreme financial pressures on mega-projects. |

| Calcasieu Pass LNG | Operational / Insurance Issues | Faced a major setback when insurer Chubb reportedly ceased its $1.5B policy in May 2025, highlighting growing insurability risk for Gulf Coast assets. |

| Plaquemines LNG | Financed | Secured financing from a global consortium of over 20 banks, including Bank of China, ING, Mizuho, and MUFG, demonstrating continued appetite for major U.S. LNG projects. |

Four Levers to De-Risk and Decarbonize

To de-risk these interconnected risks, LNG projects can pursue several strategic pathways to enhance resilience and reduce their climate footprint.

| Strategy | Description & Key Measures | Potential Impact | Implementation Challenges |

|---|---|---|---|

| Methane Abatement | Implementing technologies to reduce methane emissions across the supply chain, including Leak Detection and Repair (LDAR) programs, upgrading equipment, and reducing flaring. | Highly cost-effective. The IEA reports over 60% of LNG supply chain emissions could be cut with current tech. Reducing leaks alone could cut emissions by 90 Mt CO2e, with half at no net cost. | Discrepancy between industry reporting and higher satellite measurements of leakage. Implementing comprehensive MRV systems is complex and costly. |

| Electrification of Liquefaction | Replacing gas-fired turbines with electric motors (e-drives) powered by low-carbon electricity from the grid. | Reduces on-site (Scope 1) combustion emissions by over 90% and can increase net production by over 6.5%. Reduces exposure to carbon taxes. | High upfront capital cost. Creates reliance on electrical grids that are vulnerable to hurricanes, creating a resilience trade-off. |

| Carbon Capture & Storage (CCS) Integration | Capturing CO2 emissions from gas processing and liquefaction and storing them underground. | Critical for decarbonization. Rio Grande LNG aims to capture >5M tonnes of CO2 annually, reducing emissions by >90%. A DOE study shows a ‘High CCS’ scenario results in minimal net global GHG increase. | High cost of capture technology, though costs are expected to decline. Requires suitable geological storage sites and a supportive regulatory framework. |

| Sourcing Verified Low-Leakage Gas | Ensuring the natural gas supply has a verifiably low methane footprint through robust MRV systems from wellhead to plant. | Essential for maintaining access to premium markets like the EU. Allows for marketing of ‘responsibly sourced’ gas, which can command higher prices. | High complexity and cost of implementing a credible, independently verified MRV system across a commingled gas network. |

Leave a Reply