The Affordable Care Act (ACA) brought significant changes to health insurance in the U.S. One major change was the introduction of benchmark premiums, especially for the Silver plan tier.

This act aimed to make health insurance more affordable and accessible, setting a standard for how premiums are calculated and adjusted based on various factors such as age, location, and coverage level.

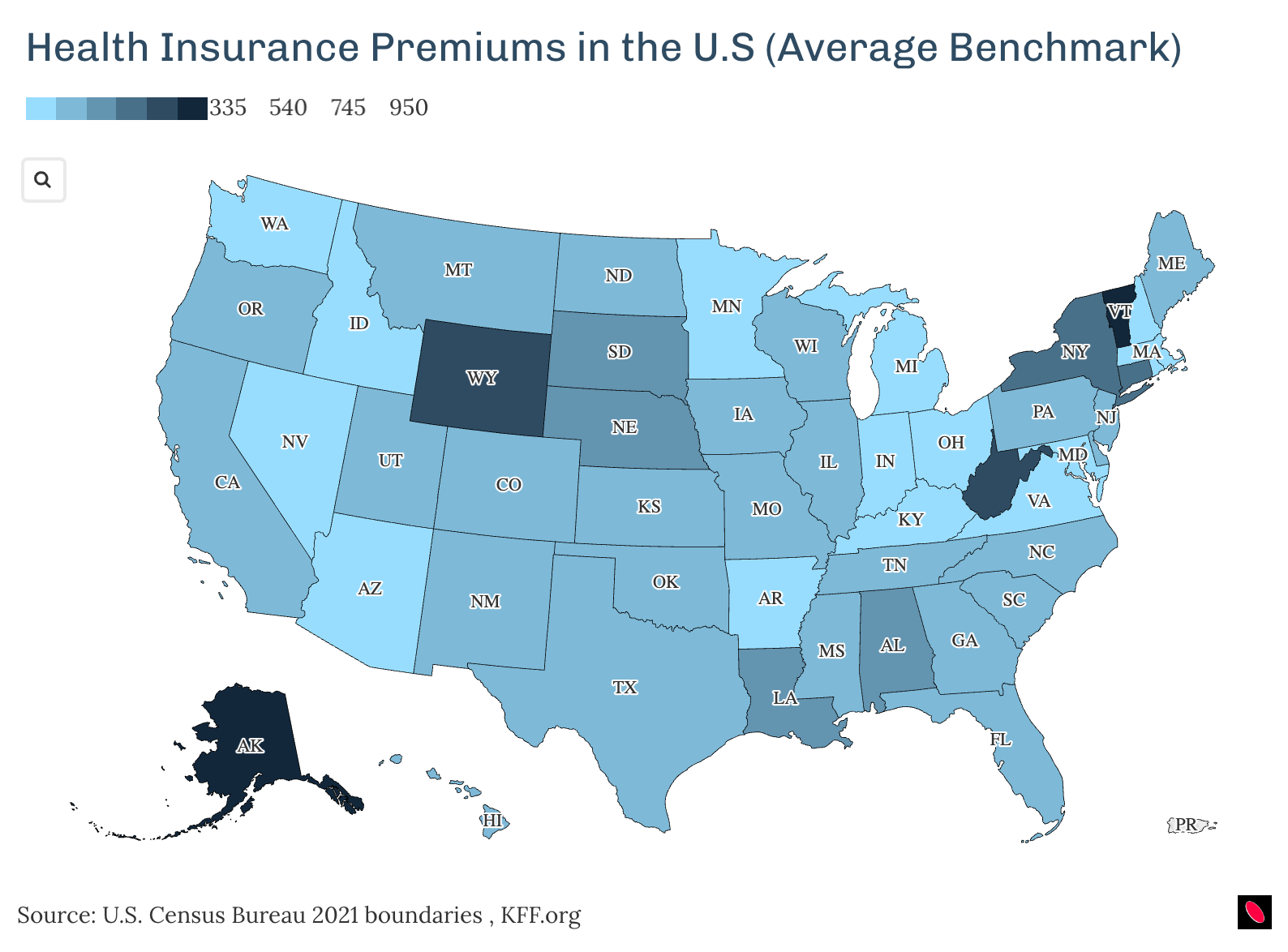

Average Benchmark Premiums by State in 2024

Note: This is an interactive map. Please hover your mouse/ tap areas on the map to view data for each state

Most Expensive States for Healthcare

When looking at the most expensive states for healthcare, it’s clear that some areas consistently have higher average benchmark premiums. States like California and Massachusetts are prime examples.

High Benchmark Premiums: California and Massachusetts

- California: The average benchmark premium in California is significantly higher compared to many other states. This can be attributed to several factors, including a large population, diverse demographics, and a high cost of living.

- Massachusetts: Known for its advanced healthcare system, Massachusetts also ranks high in terms of benchmark premiums. The state’s emphasis on comprehensive coverage and robust healthcare infrastructure contributes to these elevated costs.

Contributing Factors to Higher Costs

Several elements influence the higher benchmark premiums in these states:

- Provider Shortages: In states like California, a shortage of healthcare providers leads to increased competition for services, driving up costs.

- High Demand for Services: Both California and Massachusetts have high demand for specialized medical services, which often come with higher price tags.

- Cost of Living: The general cost of living in these states is higher, which translates into increased operational costs for healthcare providers.

Least Expensive States for Healthcare

When it comes to the least expensive states for healthcare, places like North Carolina and South Dakota often stand out. These states are known for having some of the lowest average benchmark premiums, providing a more affordable option for many residents.

States with Lowest-Cost Premiums

Here are the states with the lowest-cost premiums:

- North Carolina: Known for its competitive insurance market, North Carolina offers relatively low premiums compared to other states. The competition among insurers helps to keep prices down while maintaining a variety of plan options.

- South Dakota: This state benefits from a generally healthy population, which contributes to lower healthcare costs. Additionally, the lower demand for healthcare services compared to more densely populated areas helps keep premiums affordable.

Factors Influencing Lower Healthcare Costs

Several factors contribute to the lower healthcare costs in these states:

- Competition Among Insurers: In states like North Carolina, multiple insurance providers compete for customers, driving down premium costs.

- Healthier Populations: States such as South Dakota generally have healthier populations, which leads to lower utilization of healthcare services and thus reduced costs.

- Lower Demand for Services: Less densely populated areas often experience lower demand for healthcare services. This reduced demand can lead to more affordable premium rates.

Age-Based Premium Variations

Age significantly impacts health insurance premium rates. Younger individuals typically benefit from lower premiums, while older adults often face higher costs. For example, a 40-year-old’s premium rate can be substantially less than that of a 60-year-old, reflecting the increased risk insurers associate with aging.

Comparison of Average Premiums Across States

Younger Individuals

- In New York, a 25-year-old might pay around $350 monthly for a silver plan.

- In Texas, the same individual could see rates closer to $300.

Older Individuals

- A 60-year-old in Florida may encounter premiums upwards of $700.

- Conversely, in Ohio, this age group might find rates around $650.

County-level premium data further reveals disparities within states. For instance:

- California: Los Angeles County shows lower premiums for all age groups compared to rural counties like Humboldt.

- Illinois: Cook County offers more competitive rates than less populated areas such as Alexander County.

Leave a Reply