The average American homeowner currently pays about $2,110 annually, or $176 monthly, for homeowner’s insurance.

This national average serves as our baseline, but like weather patterns across our vast country, insurance costs vary dramatically depending on where you live.

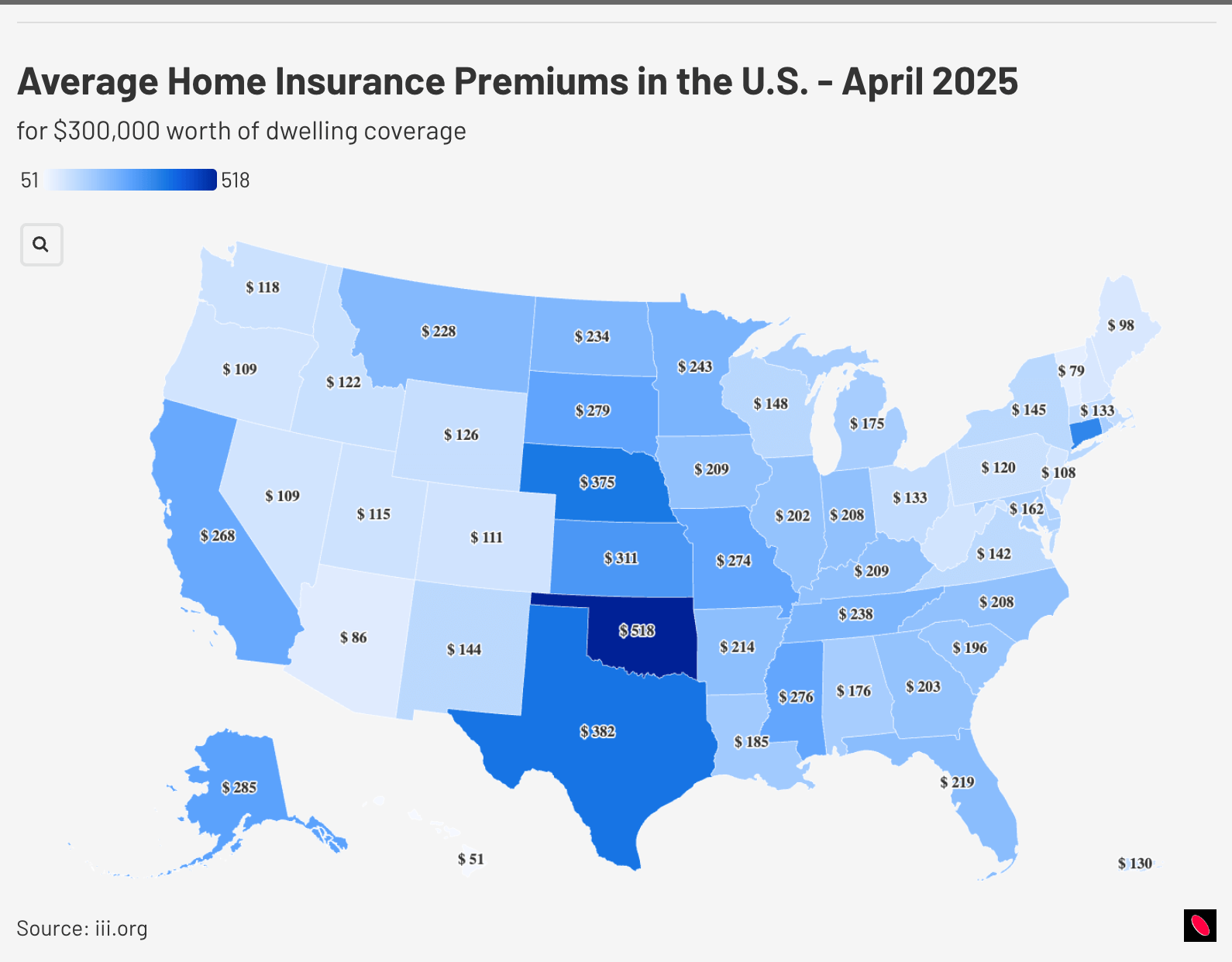

This is an interactive map. Hover on the states to reveal additional information.

Why Such Big Differences?

Homeowner’s insurance costs across states range from as low as $610 annually in Hawaii to a staggering $6,210 in Oklahoma. These variations aren’t arbitrary, but rather reflect the unique risk profiles of different geographical areas.

The Most Expensive States

- Oklahoma leads the nation at $6,210 annually ($518 monthly), largely due to its position in “Tornado Alley” and frequent exposure to severe weather events. This is nearly three times the national average—imagine paying for three insurance policies while your neighbor in another state pays for just one.

- Texas follows at $4,585 annually ($382 monthly), where the perfect storm of hurricane risks along the Gulf Coast, tornado exposure in northern regions, and hail damage throughout the state creates a challenging insurance environment.

- Nebraska rounds out the top three at $4,505 annually ($375 monthly), with tornadoes, hailstorms, and severe winter weather contributing to its high premiums.

- Colorado ($4,175 annually/$348 monthly) faces high costs due to wildfire risks, hailstorms, and the growing expense of rebuilding in its booming housing markets.

The Most Affordable States

- Hawaii offers the nation’s lowest rates at just $610 annually ($51 monthly)—less than a third of the national average. The Aloha State’s limited exposure to tornadoes and freezing weather helps keep costs down, though hurricane and volcanic risks still exist.

- Vermont ($950 annually/$79 monthly) benefits from lower population density and fewer catastrophic weather events.

- Delaware ($1,025 annually/$85 monthly) and Alaska ($1,035 annually/$86 monthly) also provide relatively affordable coverage options.

Cost Drivers

- Natural Disaster Frequency: States prone to hurricanes (Florida, Texas), tornadoes (Oklahoma, Kansas), wildfires (California, Colorado), or floods (Louisiana) generally have higher premiums.

- Construction Costs: Areas with higher rebuilding costs push insurance premiums upward. This explains why some states with moderate risk profiles still have higher-than-expected rates.

- Home Values: More expensive homes typically require more coverage, influencing average state rates.

- Population Density: Urban centers often have higher claim frequencies, which can drive up rates.

- State Regulations: Different regulatory environments affect how insurance companies set rates and manage risk.

Regional Factors

The Midwest

The Midwest presents a study in contrasts. While states like Ohio ($1,590 annually) offer relatively affordable coverage, others like Nebraska ($4,505) and Kansas ($3,735) face much steeper costs. The dividing line often comes down to tornado risk exposure—like a game of weather roulette that some states consistently lose.

Coastal States

Surprisingly, not all coastal states face exorbitant rates. While Florida’s $2,625 annual premium reflects its hurricane exposure, California’s relatively modest $1,335 annual cost might seem unexpected given its size and natural disaster risks. This difference partly stems from California’s regulatory environment and the fact that earthquake coverage is typically purchased separately from standard homeowner’s policies.

Mountain States

The mountain region shows considerable variation, with Colorado ($4,175) facing much higher costs than its neighbor Utah ($1,385). This disparity often relates to recent claim histories and different exposures to specific risks like hailstorms and wildfires.

What This Means For Homeowners

For homeowners in states with premiums significantly above the national average, consider:

- Increasing deductibles to lower premiums

- Bundling policies for potential discounts

- Investing in home hardening measures that might qualify for premium reductions

- Comparing quotes from multiple carriers, as pricing can vary significantly

Looking Ahead

Climate change continues to affect weather patterns and disaster frequencies, potentially shifting costs in coming years.

Areas previously considered low-risk may face new challenges, while advancements in construction and mitigation techniques could help reduce risks in traditionally high-cost regions.

Understanding where your state stands can help you budget appropriately and make informed decisions about your coverage.

Leave a Reply